Practical Financial Advice

Practical Financial Advice

Money don't get everything, it's true. But what it don't get, I can't use, I need money (That's what I want)

When I was in the navy it was widely understood that many of the youngest members of the junior ranks had no idea how to handle their finances. The situation was so terrible that it was said half-jokingly that if they had checks in the check book, they thought it meant they still had money in the bank. This should not have come as a surprise as these young men and women were mostly fresh out of high school and the schools did little to prepare them for the real world. To the best of my knowledge the education system still does little if anything to prepare graduates for real world finances. Even worse, the financial world has become more complicated. When I graduated from college, finances seemed to be limited to savings accounts, checking accounts, credit cards, and RRSPs (that’s like a 401k for you Americans). Since then, we’ve added the Tax-Free Savings Account or TFSAs (that’s like a Roth IRA) and thrown the internet into the mix. Sure, the internet is convenient and provides transparency, but if you don’t know what you’re doing, the “inconvenience” of having to go down to the bank and talk with someone can prevent you from making some serious mistakes.

I put it all into NFTs…or bitcoin…or magic beans. They’re all good, right?

Managing finances and investing can be intimidating, but it needn’t be. We don’t all need to know the details of a Long Butterfly option strategy to get our financial houses in order – ya I Googled it, sue me.

https://commons.wikimedia.org/wiki/File:Long_butterfly_option.svg#/media/File:Long_butterfly_option.svg

{kind=link}

There are two caveats for the following advice to be useful:

1. You need money.

2. You can’t have too much money.

The first requirement can be summed up as follows: you need to spend less than you earn. It’s sounds simple and yet so many people struggle with it. Think about things you can live without. Certainly not this blog…maybe cut back on what you spend on your kids. What have they ever done for you anyway?

The second requirement for this advice to be useful is that you can’t have too much money. Is there such a thing? While Wallace Simpson once said, “you can never be too rich or too thin,” for the purposes of this advice it is possible to be too rich. You’ll know you have too much money for this advice to be useful if you can answer these three questions:

1. Where to get a gold-plated bidet cleaned?

2. What is polo? If you answered Spanish for chicken, you’re not rich.

3. Which arm should you use to beat your valet? (The answer is your non-check writing arm. Duh!)

If you got all of these correct you have too much money for me to help you and you should do two things:

Buy a subscription to my Substack

Go do a Scrooge McDuck

In 2022 the estimated revenue of the financial services industry in the United States was US$4962 billion. A lot of people clearly value the advice from this sector but as my old memaw used to say (fictional account and person), everything you need to know you can get from old sayings. So here you go:

“Save for a rainy day” – Aesop. Put aside 10% of what you earn (pay yourself first) and have 6 months’ worth of salary in the bank.

“A Penny Saved is a Penny Earned” – Money you don’t spend is just as valuable as money you earn. There are two ways to get ahead, earn more or spend less.

“Waste not, want not” – Similar to the previous but specifically aimed at what you’ve purchased. If you eat leftovers occasionally you won’t have to spend as much money on groceries (to use one example).

“Never spend your money before you have it” —Thomas Jefferson. The possible exception to this is cash back credit cards. Getting 1% back on every purchase adds up. Just make sure you pay off the balance every month, so you don’t get hit with interest payments.

“A fool and his money are soon parted” and “if it sounds too good to be true it probably is” – if you don’t understand it, don’t invest in it. Cough, cough, NFTs and Bitcoin.

“There’s no such thing as a free lunch” – A saying that’s best remembered when talking to financial advisors. Remember to ask how they make their money. I’m sure you’re lovely, but the only reason they’re helping you is to help themselves and if it comes down to you or them guess which one it’s going to be.

Take care of the little things and the big things will take care of themselves. – Emily Dickinson. Read as it stands it would seem to imply that if you worry about the little expenses the big ones will take care of themselves. However most people forget the second half of this quote, “You can gain more control over your life by paying closer attention to the little things.” Track what you spend!

“Penny wise and pound foolish” – the caveat to #7 above is #8. Don’t be careful and economical in small matters while being wasteful or extravagant in large ones.

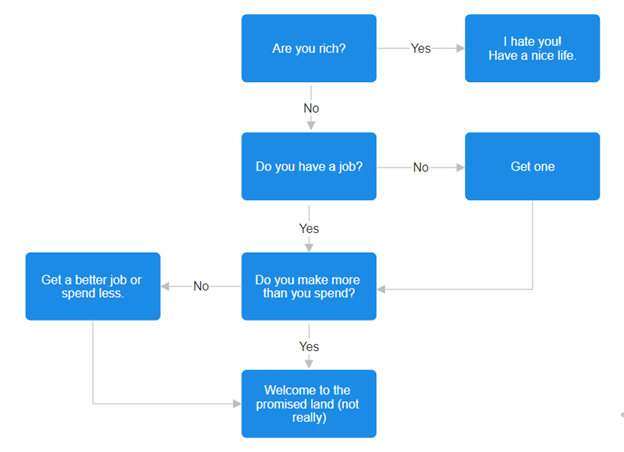

If your goal is to get rich quick, good luck to you. I will happily advise you for 1% of your profits (and 0% of your losses). If your goal is to slowly accumulate savings, you could do worse than spending less than you make, only buying what you can pay for immediately, and investing cautiously. This may sound boring, but I assure you it’s much worse; it’s boring and hard work (unless you like spreadsheets as I do in which case, tally ho, nerd). Bear in mind though, if you find yourself taking off your shoes and socks to count to eleven, maybe talking to a financial advisor wouldn’t be the worst move you could make.

Finally, while money is important it’s not everything. Is it the root of all evil? I don’t think so. It is a tool, a means of acquiring what we need and sometimes what we don’t need but really want. Can it buy happiness? Most would say “no,” but opinions are divided:

Charles Dickens - Annual income 20 pounds, annual expenditure 19 [pounds] 19 [shillings] and six [pence], result happiness. Annual income 20 pounds, annual expenditure 20 pounds ought and six, result misery.

Groucho Marx - Money can’t buy happiness but it’ll buy the kind of misery you can enjoy.

I think Groucho was probably closer to the truth.

I have done my best to provide you with some simple, if somewhat folksy, financial advice. Some might argue that I am too focused on budgets, too cautious, that I “know the price of everything but the value of nothing.” There are, of course, two sides to every debate and so I will let that old reprobate Oscar Wilde give the opposing view: “anyone who lives within their means suffers from a lack of imagination.”

The thrift admonitions are very important, especially never taking on unsecured debt.

Alas, the single most important aspect of becoming financially secure is not thrift. It is having a high enough income to make saving worthwhile (the "Get a better job ... " process rectangle).

One can net an additional $20,000 annually more readily than one can save $20,000/year from, say, a $50,000 income. Like living within one's means, targeting and achieving a particular income involves hard choices, may require deferral of gratification, requires a relentless realism.

The odd janitor who lives alone and saves every penny may die a millionaire, but in general, income is the foundation underpinning saving. There are certainly people who have high incomes who don't save effectively. However, with a very low income, there is not enough to compound investments. Magnitude of saving is more important than percentage. (Starting as early as possible with whatever is available is of course also important, to reap the benefit of compounding.)

---

I agree that fiscal education should be taught. I do lean toward a conspiracy-type suspicion that such knowledge is intentionally withheld, given how micromanaged curriculum is. Also, teachers and admin are government employees. They teach people how to be government employees. The few teachers who have had other careers tend to have very different attitudes than those who obtained education degrees.

---

(Personally, I wish for the author that Substack becomes a viable income stream! There is always piracy as a fallback.)